Government Notifies 31 July 2026 as Extended Due Date for Filing GSTAT Appeals and Applications under CGST Act

The Goods and Services Tax Appellate Tribunal (GSTAT) is a creature of statute and is strictly bound by the timelines mandated under the Central Goods and Services Tax (CGST) Act. It possesses no inherent or equitable power to entertain an appeal filed beyond the absolute outer limit allowed by law. A discretionary delay of up to an additional 3 months can be condoned by the Tribunal if sufficient cause is demonstrated.

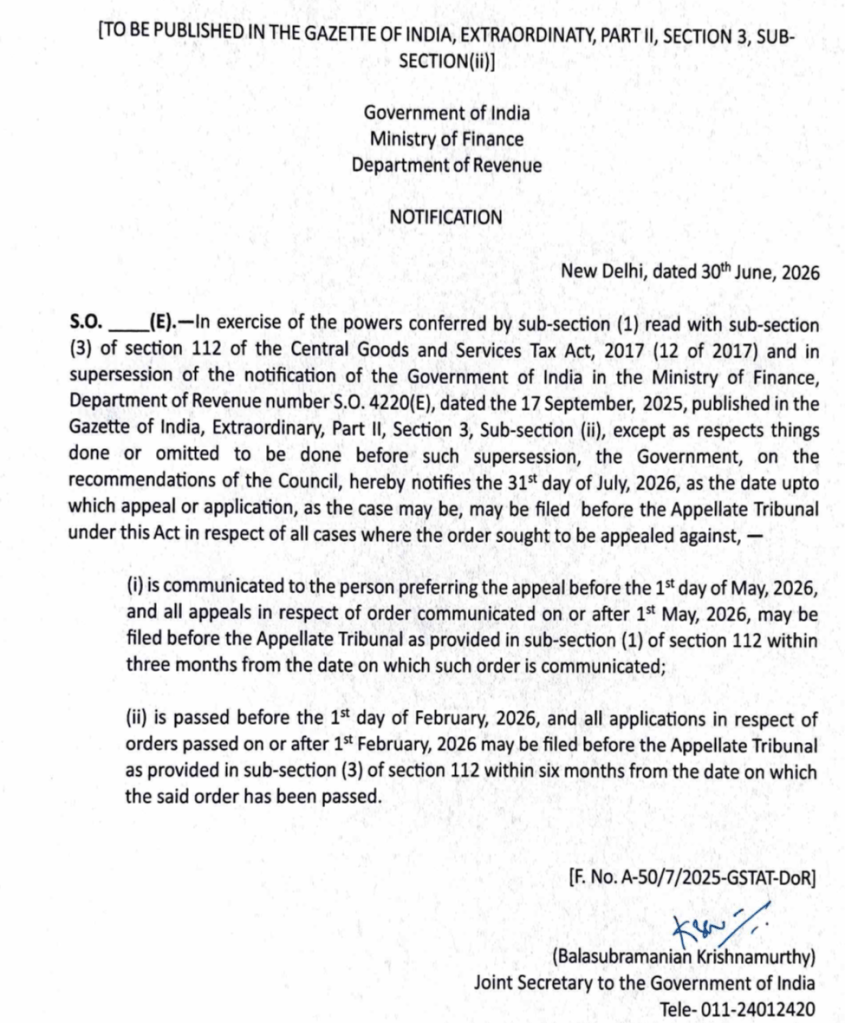

Tax professionals, industry bodies and bar association urge Finance Ministry to extend June 30 cut-off, citing technical issues on GSTAT portal.

GSTAT portal had been launched by the Hon’ble Finance Minister on September 24, 2025. An Order F. No. GSTAT/Pr. Bench/Portal/125/25-26 dated 24.09.2025 was issued to direct a staggered mode of filing appeals before GSTAT in order to avoid any portal related glitches.

The time-limit for filing appeal for orders is released on the basis of date of order uploaded on the GST portal was set as per the following manner:

| S. No. | Appeals (APL-01/ APL-03) filed on the GST Portal by Assessee or Department or Revisions (RVN-01) issued on the GST portal | Period during which appeal in GST Form APL-05 may be filed |

| 1. | Order issued on or before 31.01.2022 | Appeal could be filed from 24.09.2025 to 31.10.2025 The last date of filing appeal continues to be 30.06.2026 |

| 2. | Order issued on or after 01.02.2022 but on or before 28.02.2023 | Appeal could be filed from 01.11.2025 to 30.11.2025 The last date of filing appeal continues to be 30.06.2026 |

| 3. | Order issued on or after 01.03.2023 but on or before 31.01.2024 | Appeal could be filed from 01.12.2025 to 31.12.2025 The last date of filing appeal continues to be 30.06.2026 |

| 4. | Order issued on or after 01.02.2024 but on or before 31.05.2024 | Appeal could be filed from 01.01.2026 to 31.01.2026 The last date of filing appeal continues to be 30.06.2026 |

| 5. | Order issued on or after 01.06.2024 but on or before 31.03.2026 | Appeal can be filed from 01.02.2026 to 30.06.2026 The last date of filing appeal continues to be 30.06.2026 |

| 6. | Order issued on or before 31.03.2026 | Appeal can be filed from 01.03.2026 upto 30.06.2026 The last date of filing appeal continues to be 30.06.2026 |

The RBI circular dated April 22, 2025, mandated that all scheduled commercial and cooperative banks migrate to the .bank.in domain by October 31, 2025. However, this is not a sudden shift, many banks began operations, phased integrations, and user-awareness campaigns running into 2026 to ensure a completely seamless and secure transition without disrupting access.

The .bank.in domain is managed by the Institute for Development and Research in Banking Technology (IDRBT) and strictly implements advanced security protocols, including DNSSEC and high-assurance certificates.

What remains unchanged?

This is a great initiative by Reserve Bank of India to reduce digital frauds and to make banking websites more secure & easily recognisable for customers.

Goods and Services Tax Network (‘GSTN’) has extended the rollout date for mandatory capture of Ship-To GSTIN in Bill-To Ship-To transactions and voluntary closure of e-way bill functionality from June 15, 2026, to August 1, 2026. Taxpayers, GST Suvidha Providers and other stakeholders have been advised to complete system changes, testing and operational preparedness before the revised date. This is a relief to tax-payers as they get additional time for integration and testing purposes.

This is a landmark development in Indian labour law that carries immediate compliance implications for organizations. The Ministry of Labour and Employment has formally notified the Central Rules under all four Labour Codes on 08 May 2026.

In November 2025, IMF the rupee from “stabilized” to “crawl-like,” indicating the RBI likely manages it to move slowly, rather than floating freely.

The IMF acts as an advisor and overseer of member country economic policies. It reclassifies regimes based on actual behavior (de facto) rather than declared policy.

A “crawl-like arrangement” means the currency remains within a 2% band relative to a statistically identified trend for six months or more, implying the RBI allows a measured, gradual depreciation rather than a freely floating rate.

The IMF observed in its 2025 assessment that the rupee showed a predictable, narrow, downward trend rather than reflecting pure market forces.

As part of the Reserve Bank of India’s updated framework under the Foreign Exchange Management (Guarantees) Regulations, 2026, dated January 06, 2026, new reporting obligations have been introduced for all guarantees involving cross‑border parties. These requirements are effective from Quarter ended March 2026

Reporting Requirements

Under Clause 7 of the FEMA regulation, reporting is mandatory for all cross‑border guarantees (BGs) that are issued, received, amended, or invoked by the client, when acting as a creditor, debtor, or surety, unless already reported by the Authorized Dealer (AD) bank.

The responsible party must ensure reporting within the prescribed timelines. Reporting must be submitted to your AD bank every quarter, within 15 days from the end of the quarter. Delayed reporting will attract a Late Submission Fee (LSF) as per RBI guidelines.

Who Must Report?

1. Surety / Guarantor (Resident in India)

If you as a resident entity are providing the guarantee.

Example: A resident corporate issuing a guarantee in favor of an overseas entity.

2. Principal Debtor / Applicant (Resident in India)

If you (Principal Debtor) have arranged a guarantee wherein the surety is a non-resident.

Example: A guarantee issued by an overseas parent or bank for credit facilities availed in India.

3. Creditor / Beneficiary (Resident in India)

If both the surety and principal debtor are non-residents, or if you have arranged the guarantee.

Example: Receipt of a guarantee from a foreign bank for obligations of an overseas entity.

Reserve Bank of India (Commercial Banks – Credit Risk Management) – Amendment Directions, 2025

Please refer to Reserve Bank of India (Commercial Banks – Credit Risk Management) Directions, 2025 dated November 28, 2025 (hereinafter referred to as ‘the Directions’).

2. On a review, in exercise of the powers conferred by the sections 21 and 35A of the Banking Regulation Act, 1949 and all other provisions / laws enabling the Reserve Bank of India (hereinafter called the Reserve Bank) in this regard, the Reserve Bank being satisfied that it is necessary and expedient in the public interest so to do, hereby issues the Amendment Directions hereinafter specified.

3. The Amendment Directions modifies the Directions as under:

(1) Chapter XI – ‘Opening of Current Accounts and CC / OD Accounts by Banks’ of the Directions shall be deleted and substituted with a new chapter as under:

Chapter XIA – Maintenance of Cash Credit Accounts, Current Accounts and Overdraft Accounts by Banks

91A. Current Accounts, Cash Credit Accounts (CC), and Overdraft Accounts (OD) may all be used as transaction accounts by the customers, which raises concerns relating to credit monitoring by the lenders. With a view to strengthening credit discipline and facilitating better monitoring of transactions and utilisation of funds, this Chapter provides a framework for maintaining such accounts banks.

A. Cash Credit Accounts

91B. CC account is operationally different from a current account or OD account, given its primary nature as a working capital facility linked to the value of the borrower’s current assets. A bank may provide such cash credit facilities as per the needs of the customer, without any restriction under this Chapter.

B. Current Accounts and OD Accounts

91C. A bank may maintain current account or OD account without any restriction in case of customers where the aggregate exposure of the banking system to the customer is less than ₹10 crore.

Explanation (1): ‘Banking System’ for the purpose of this Chapter shall include Commercial Banks (including Small Finance Banks, Local Area Banks, and Regional Rural Banks, but excluding Payments Banks), Urban Co-operative Banks and Rural Co-operative Banks (State Co-operative Banks and Central Co-operative Banks).

Explanation (2): ‘Exposure’ for the purpose of this Chapter means the sum of all sanctioned fund-based credit facilities and non-fund-based facilities availed by the borrower from the banking system.

91D. In case of customers to whom the exposure of the banking system is ₹10 crore or more:

(1) A bank may maintain current accounts or OD accounts as per the needs of the customer provided that the bank has either:

Provided that, in case no bank within the banking system meets the above criteria, or only one bank meets the above criteria, two banks from the banking system having the largest exposures to the borrower may maintain current accounts or OD accounts.

Provided further that, in case where only one bank within the banking system has any exposure to the borrower, one more bank of the customer’s choice within the banking system may maintain current accounts, subject to furnishing of a no-objection certificate (NOC) from the bank that has the exposure to the borrower.

Provided further that, in case where no Scheduled Commercial Bank (SCB) meets the above criteria, but the borrower nevertheless desires to have a current account with an SCB, such borrowers may maintain current accounts with any one SCB of their choice, subject to furnishing of NOCs from all lending banks within the banking system.

(2) A bank, not meeting the eligibility criteria at paragraph (1) above , may maintain only collection accounts.

Explanation: ‘Collection Account’ for the purpose of this Chapter means a current account or OD account used primarily for receipts of cash inflows of the accountholder. Restricted payments / cash outflows from such account shall be subject to the conditions outlined in paragraph 91F of these Directions.

91E. With a view to ensuring credit discipline, lenders may include additional covenants as per their policies in their loan agreements in mutual agreement with borrowers.

C. Collection Accounts

91F. Funds credited into a collection account shall be remitted within two working days of receipt of such funds to a CC account, current account, or OD account maintained with any bank in the banking system and designated by the borrower for this purpose (hereinafter referred to as ‘designated account’ in this Chapter). Any disbursement of overdraft limit from an OD account, which is in the nature of a collection account, shall be through the designated account only.

Provided that statutory dues such as taxes, and dues, if any, to the bank maintaining the collection account may be debited before remitting the funds.

D. Exemptions

91G. The restrictions placed in terms of paragraph 91D(1) of these Directions shall not be applicable to the accounts mentioned below:

(1) Accounts opened as per the provisions of Foreign Exchange Management Act, 1999 (FEMA) and notifications issued thereunder, including accounts mandated for ensuring compliance under the FEMA framework.

(2) Specific accounts or transactions which are stipulated under a statute or a specific instruction of a financial sector regulator, or the Central Government or a State Government.

Explanation: ‘Financial sector regulator’ for the purpose of this Chapter refers to the Reserve Bank of India (RBI), the Securities and Exchange Board of India (SEBI), the Insurance Regulatory and Development Authority of India (IRDAI) and the Pension Fund Regulatory and Development Authority (PFRDA).

(3) Accounts of entities regulated by a financial sector regulator, used for the purpose of carrying out their regulated activities.

Provided that banks operating the above-mentioned exempted accounts shall ensure that transactions in such accounts are used only for the permitted / specified purposes. Surplus funds, if any, in such accounts shall be remitted to the designated account.

91H. Banks, in certain cases, offer products or services that inherently require routing transactions through a current account maintained with themselves. In such cases, banks which are otherwise not eligible to maintain accounts in terms of paragraph 91D(1) of these Directions may also maintain current accounts, subject to the conditions specified below:

(1) Such accounts shall only be opened in accordance with a Board-approved policy for the product / service, which shall detail and justify, inter alia, the necessity of operating these accounts.

(2) Transactions in such accounts shall be limited for the specified purpose(s). Cash transactions, debits at the discretion of customers, and issuance of instruments like electronic cards and cheque books shall not be permitted in such accounts. Surplus funds, if any, in such accounts shall be remitted to the designated account.

(3) Banks shall implement adequate safeguards to ensure that such accounts are not used as substitutes for current accounts, or employed to circumvent restrictions placed on current accounts, or misused for activities such as fund diversion or fraud.

E. Compliance Monitoring

91I. For the purpose of ensuring ongoing compliance with this Chapter, all banks shall monitor accounts maintained with them on a regular basis, and in any case at least once every half-year.

91J. In case it is observed that a bank is no longer eligible to maintain a current account or OD account opened in terms of:

(1) paragraph 91C due to increase in exposure of banking system to the borrower up to or beyond the specified threshold of ₹10 crore; or

(2) paragraph 91D(1), due to changes in the bank’s share in banking system’s aggregate exposure or in aggregate fund-based exposure to the borrower; or due to non-availability of NOC from banks that have exposure to the borrower;

then the bank shall notify the customer(s) concerned promptly, and in any case within one month from the date of observing such ineligibility, that the account must either be converted to a collection account or closed. The conversion or closure process, as the case may be, shall be completed within three months of observing such ineligibility.

91K. Accounts opened in terms of these Directions shall be appropriately flagged in the bank’s core banking solution (CBS) to ensure clear identification and to facilitate effective monitoring. Banks maintaining multiple accounts for a borrower shall ensure that such accounts and transactions and cashflows therein are monitored at the borrower level as also at the account level.

F. Other Provisions

91L. A bank shall ensure that an accountholder utilize their account solely for transactions related to their authorized business or activities. These accounts shall not, under any circumstances, be used as pass-through channels for facilitating third-party transactions.

Provided that entities expressly licensed or authorized by a financial sector regulator to facilitate third-party transactions may continue to do so. However, such activities shall strictly be limited to the specific transactions they are authorized to do and shall not extend beyond that scope. Any account that has been permitted to carry out such third-party transactions shall be appropriately flagged in the bank’s CBS to ensure clear identification and to facilitate effective monitoring.

91M. A bank shall ensure that an accountholder, who is not licensed or authorized by the Reserve Bank to accept deposits or to provide payment services, do not engage in such activities through accounts maintained with them.

91N. Robust monitoring systems shall be implemented to detect the above prohibited usage, including mechanisms to flag accounts exhibiting unusually high transaction volumes, frequent pass-through activities, or inconsistencies between the accountholder’s stated line of business and transactions carried out through the account.

91O. Term loans sanctioned by the bank shall preferably be remitted directly to the intended beneficiary’s account(s) or for the specified end-use, where such beneficiary is identifiable, rather than routing the funds through the borrower’s account.

4. The above amendments shall come into force from April 1, 2026. Banks may however decide to implement the amendments in entirety from an earlier date.

In case of The Hongkong and Shanghai Banking Corporation Ltd Vs State of Maharashtra, Hon’ble Bombay High court held that GSTAT possesses inherent and incidental power to grant interim relief, including stay of recovery during pendency of appeal. Assessee must seek relief before Tribunal instead of filing Writ Petition in High Court.

The Reserve Bank of India (RBI) has notified the Foreign Exchange Management (Borrowing and Lending) (First Amendment) Regulations, 2026 (Notification No. FEMA 3(R)(5)/2026-RB, dated February 9, 2026, and published in the Official Gazette on February 16, 2026).

Key Highlights of the Amendments

1. Expanded Eligible Borrowers and Recognized Lenders

• Broader inclusion of entities (e.g., any person resident in India except individuals, subject to incorporation/registration under applicable laws).

• Enhanced recognition of foreign lenders to increase funding options.

2. Revised Borrowing Limits

• Eligible borrowers can now raise ECBs up to the higher of:

• USD 1 billion (outstanding ECBs), or

• Total outstanding borrowings (external + domestic) up to 300% of net worth (based on the last audited standalone balance sheet).

3. Removal of Cost of Borrowing Restrictions

• All-in-cost ceilings (previously benchmark + margin) have been removed.

• Pricing is now fully market-driven.

• For refinancing, the earlier requirement of lower cost/credit spread has also been eliminated.

4. Rationalized Minimum Average Maturity Period (MAMP)

• Uniform MAMP of 3 years for most ECBs.

• Manufacturing sector borrowers: MAMP between 1–3 years, subject to outstanding ECB ≤ USD 150 million.

• Longer maturity requirements (e.g., 5/7/10 years in older tracks) have been streamlined or removed.

5. Refinancing Provisions

• Refinancing (full or partial) of existing ECBs by fresh ECB is permitted.

• Safeguard: Refinancing must not result in failure to meet the MAMP requirement applicable to the original borrowing (or weighted outstanding maturity for multiple borrowings).

• This allows flexibility in rollovers while preventing undue shortening of the original maturity profile.

6. Strengthened End-Use Restrictions (New Regulation 3A)

• Detailed prohibitions/restrictions introduced to prevent misuse, including:

• Investment in chit funds, Nidhi companies.

• Real estate business (with limited exceptions, e.g., clarified for land/immovable property in permitted cases).

• Capital market transactions (except certain strategic corporate actions).

• On-lending restrictions in some cases.

• Repayment of certain restricted domestic loans or NPAs.

• End-uses now more tightly monitored for productive purposes.

7. Simplification of Reporting and Compliance

• Streamlined requirements (e.g., updated forms, event-based reporting via ECB-2).

• Enhanced clarity on security creation, conversion to non-debt instruments, corporate actions.